Every owner dreams of the moment when they step away from their business, having achieved financial freedom and prepared for what comes next. Yet for many, that moment arrives with an unpleasant surprise. The average net worth at exit is approximately $15 million, but taxes can claim a larger share than expected, reducing what was intended to secure the future.

After decades of building value, few owners realize how much of it can quietly disappear through capital gains, depreciation recapture, and poorly structured deals. Years of discipline and sacrifice can unravel in a single transaction if tax planning starts too late.

In this blog, we will discuss how strategic, early tax planning can help protect the value owners have spent a lifetime creating and ensure that the rewards of success stay where they belong.

Importance of Tax Efficiency in an Exit Strategy

A business exit is often the most significant financial event in an owner’s lifetime. The right tax strategy can protect years of effort from being lost to unnecessary liabilities and position the sale for maximum net gain.

1. Minimize Exit Tax Burden

Taxes often represent the single most considerable cost during a business sale. The difference between a well-planned transaction and a rushed deal can reach millions in unnecessary losses. Without preparation, owners end up reacting to complex tax obligations rather than managing them proactively.

2. Plan Early for Control

Early tax planning gives owners control over timing, structure, and cash flow. Proper preparation helps reduce exposure, align transactions with favorable tax rates, and spread proceeds across multiple tax years, turning a single liquidity event into lasting wealth.

3. Strengthen Buyer Confidence

Buyers are drawn to well-prepared sellers. A tax-efficient exit signals professionalism, organization, and foresight, qualities that lead to smoother negotiations, reduced deal friction, and stronger post-closing outcomes.

4. Preserve Long-Term Value

Thoughtful tax planning turns a potential burden into a strategic advantage. Owners can preserve more enterprise value, maximize net proceeds, and direct wealth toward personal, family, or philanthropic goals.

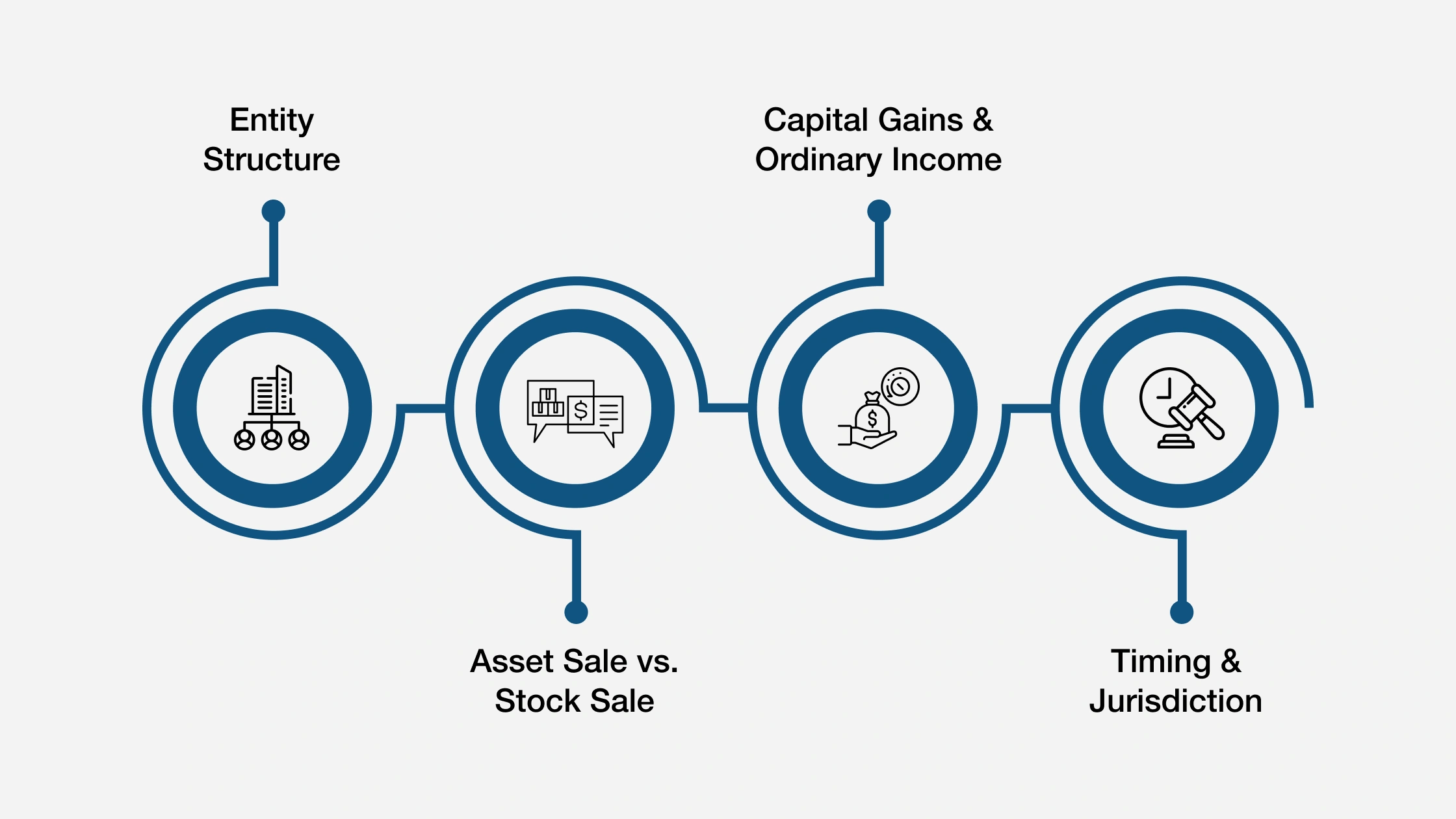

Major Tax Considerations for Business Exits

Every business exit triggers a series of tax consequences that directly affect the owner’s final payout. Understanding these implications early helps shape a strategy that minimizes tax exposure and maximizes retained value. Several key considerations determine how much an owner ultimately retains after the sale.

1. Entity Structure

The legal structure of a business, be it a C corporation, an S corporation, an LLC, or a partnership, determines how income is taxed and how sale proceeds are treated. Certain entities face double taxation when selling assets, whereas others are eligible for pass-through treatment, which can reduce the total tax burden.

Reviewing the structure years before an exit often reveals opportunities to reorganize for better outcomes.

2. Asset Sale vs. Stock Sale

The way a transaction is structured can significantly alter the tax impact. Asset sales often trigger higher ordinary income tax rates due to depreciation recapture, whereas stock or membership interest sales are typically taxed at lower capital gains rates. Each approach offers distinct benefits for buyers and sellers, making negotiation and timing crucial.

3. Capital Gains & Ordinary Income

Not all proceeds are taxed equally. Long-term capital gains generally offer lower rates than ordinary income, but qualifying for those rates depends on how long assets have been held and how the deal is structured. Planning allows owners to align their strategy with these rate differences.

4. Timing & Jurisdiction

When and where a transaction closes can influence tax liability. Changes in tax law, shifts in interest rates, and variations across state and local jurisdictions all affect final numbers. Owners who anticipate these factors can time their exit for more favorable conditions, instead of being caught off guard when it matters most.

Tax efficiency begins long before the sale. Each of these considerations works together to define how wealth moves from the business to the owner and how much remains in the process.

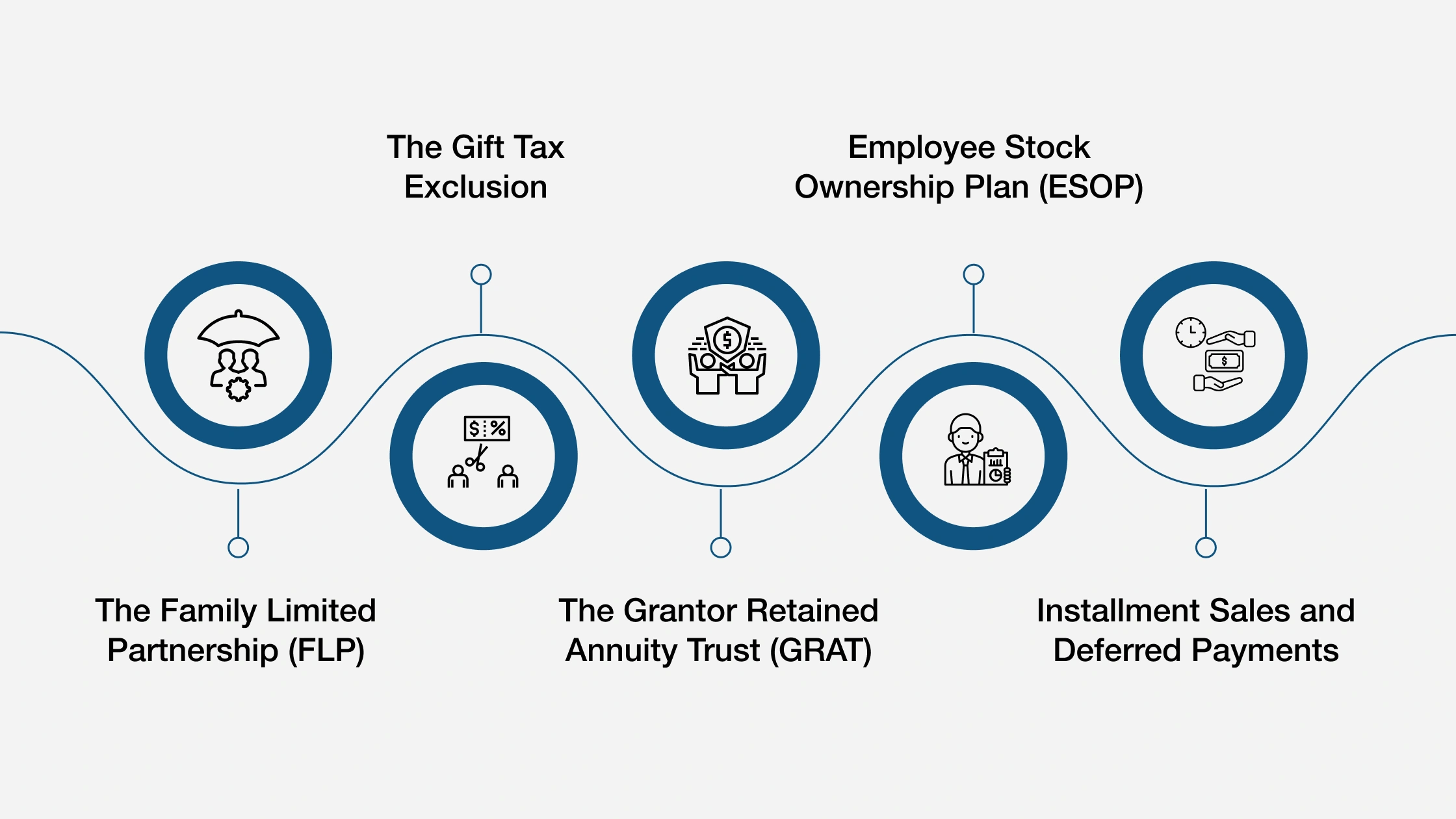

Top 5 Tax-Efficient Strategies Owners Should Consider

Once the implications of tax exposure are clear, the next step is to apply strategies that reduce liabilities and protect wealth. Many of these approaches require coordination among financial, legal, and valuation professionals, but the owner’s early awareness makes all the difference.

The most effective strategies include planning, structuring deals thoughtfully, and aligning personal and business goals before negotiations. Over time, even minor adjustments to the ownership structure, timing, or method of transfer can result in substantial tax savings.

The following strategies represent practical, widely used methods for improving tax outcomes during a business exit. Each can be tailored to the owner’s goals and timeline.

1. The Family Limited Partnership (FLP)

A Family Limited Partnership (FLP) is effective for owners who plan to transition business ownership to family members while managing gift and estate tax exposure. The arrangement enables the owner to transfer business assets to the partnership while maintaining control during the transition period.

The owner retains a small general partnership interest, often around one percent, which preserves management authority and decision-making power. The remaining limited partnership interests, usually 99 percent, can then be gradually gifted to children or other family members. These limited interests impose restrictions on control and liquidity, which can result in valuation discounts when calculating gift tax obligations.

This structure achieves two critical outcomes. It enables the owner to begin transferring ownership during their lifetime without surrendering control, and it reduces the taxable value of the estate over time. The FLP also helps protect assets from potential creditors and ensures business continuity across generations.

2. The Gift Tax Exclusion

The annual gift tax exclusion for 2025 is $19,000 per recipient, an increase from $18,000 in 2024, according to the IRS. This exclusion allows individuals to transfer up to $19,000 per person each year without affecting their lifetime gift and estate tax exemption or triggering a taxable event. For married couples who choose to “split gifts,” the total exclusion doubles to $38,000 per recipient annually.

Within an exit planning context, the annual exclusion offers a straightforward way for owners to begin transferring wealth and equity long before the sale. Gifting shares of the business to family members, trusts, or future successors can reduce the taxable estate and gradually shift ownership without triggering large tax consequences.

Used consistently over several years, these gifts can significantly reduce the value of the estate while maintaining control through structured agreements, such as grantor-retained annuity trusts (GRATs) or family limited partnerships (FLPs). Proper documentation and valuation are essential, especially when transferring non-cash assets, such as business interests, to avoid IRS scrutiny or challenges to undervaluation.

While the annual exclusion may seem modest, its cumulative impact over time can be substantial. Integrating this approach into the broader exit plan enables owners to manage wealth transfer intentionally, reduce estate exposure, and establish a more tax-efficient foundation for future generations.

3. The Grantor Retained Annuity Trust (GRAT)

A Grantor Retained Annuity Trust (GRAT) is an effective structure for transferring future business appreciation to heirs with minimal impact on estate taxes. Through a GRAT, the owner places business interests into a trust for a defined term while retaining the right to receive annual annuity payments based on the value of the assets transferred.

This approach moves the asset’s current value out of the owner’s estate, allowing any future appreciation to occur within the trust rather than under the owner’s personal ownership. When the trust term ends, the remaining value passes to beneficiaries, often children or family members, without incurring additional estate taxes.

Timing and longevity are critical to this strategy. If the owner passes away before the trust term ends, the business interest typically reverts to the estate, becoming taxable. However, with proper planning and valuation, a GRAT allows the owner to lock in a low transfer value, capture future growth tax-free, and align wealth transfer with long-term succession goals.

4. Employee Stock Ownership Plan (ESOP)

An Employee Stock Ownership Plan (ESOP) offers a structured, tax-advantaged way for owners to transition the business while rewarding the employees who helped build it. Through an ESOP, a company establishes a qualified retirement plan that purchases shares from the owner over time, funded by company contributions or external financing.

This approach provides the owner with liquidity, creates a succession path, and builds employee engagement through ownership participation. ESOPs are especially appealing because of their potential tax benefits.

Sellers of C-corporations may defer capital gains taxes by reinvesting proceeds into qualified securities, while companies operating as S-corporations under an ESOP structure can reduce or even eliminate corporate income taxes on the ESOP-owned portion.

Apart from tax advantages, an ESOP helps preserve culture and continuity. It allows employees to benefit directly from the company’s future growth while maintaining internal control. When structured carefully and supported by valuation and fiduciary oversight, an ESOP can achieve a balanced transition, protecting the owner’s financial interests and securing the company’s long-term stability.

5. Installment Sales and Deferred Payments

An installment sale allows an owner to spread the proceeds from a business sale over several years rather than receiving a lump sum at closing. This structure can be an effective way to reduce the immediate tax burden by spreading the recognition of capital gains across multiple tax years. It also creates a more predictable flow of income post-sale, which can support retirement or reinvestment plans.

Under this arrangement, the buyer pays a portion of the purchase price upfront, followed by scheduled payments with interest over time. Each payment includes both principal and interest components, and taxes are applied only to the portion of gain recognized each year. This gradual recognition may help the seller remain within lower tax brackets and better manage overall liability.

While installment sales can improve cash flow and tax efficiency, they do carry risk. If the buyer defaults or the business underperforms, the seller may face payment delays or losses. Proper documentation, collateral arrangements, and legal oversight are essential to protect both parties.

How Can Advisors Guide Tax-Efficient Exits?

Tax efficiency in an exit strategy is the result of preparation, structured analysis, and expert collaboration. Business owners rely on experienced advisors to help them understand how entity structure, valuation, and deal terms influence their after-tax outcome. The advisor’s role is to bring foresight, objectivity, and coordination to a process that involves multiple disciplines.

This is where the International Exit Planning Association (IEPA) plays a critical role. IEPA equips financial advisors, CPAs, attorneys, consultants, and part-time CFOs with the frameworks and practical education necessary to navigate the full spectrum of exit planning, including tax optimization.

Through its Certified Business Exit Consultant® (CBEC®) program, IEPA provides training based on real-world application, ensuring advisors can identify tax implications early and integrate them into the owner’s broader exit plan.

There are several benefits of being a certified exit planner. Advisors trained under the IEPA model learn how to evaluate transaction structures, time exits strategically, and align tax outcomes with client goals. Their insight transforms what could be a reactive process into a guided transition, preserving more of the business’s value while ensuring owners exit on their terms.

Make Your Business Exit Smarter & Tax-Efficient With IEPA Certification

Business owners spend decades building wealth, but without proper planning, much of it can be lost to taxes at exit. The Certified Business Exit Consultant® (CBEC®) program from the IEPA gives advisors the specialized knowledge and frameworks needed to lead tax-efficient, value-driven exits.

CBEC® certification focuses on practical application, preparing advisors to manage complex transitions with confidence and precision.

CBEC® designees achieve measurable results:

- 66% structure their client engagements in multiple phases, ensuring value delivery throughout the exit process.

- 44% work with 6–10 exit planning clients each year, demonstrating sustained engagement and active practice application.

- 22% report earning over $250,000 annually from Exit Planning services.

- 33% charge between $10,000 and $15,000 for initial planning engagements, reflecting the high professional value of their work.

The CBEC® membership helps you:

- Build stronger, tax-efficient Exit Plans that protect client wealth.

- Guide owners through valuation, structure, and timing decisions that affect tax outcomes.

- Collaborate confidently across legal, financial, and M&A disciplines.

- Elevate your advisory practice with a recognized, practitioner-led certification.

Owners deserve advisors who can help them exit successfully and keep more of what they’ve earned. CBEC® certification gives you the structure, credibility, and expertise to deliver that outcome.

Step into the next stage of advisory excellence.