A growing number of private company transactions now rely on performance-based or contingent payouts, but these structures often carry more risk than owners realize. A recent study found that less than 60% of deals with an earnout ever result in a full or even partial payment, meaning many sellers never receive the value they thought they negotiated.

This trend shows that the headline purchase price matters far less than the contract structure behind it. When payment depends on future performance, integration success, or milestones controlled by the buyer, the seller absorbs significant financial and operational risk long after the deal closes.

Many business owners enter negotiations focused on valuation, unaware that earnouts can materially reduce what they ultimately collect. Advisors who understand how these attention-based contracts shift risk are essential in helping owners protect value and negotiate terms that reflect real-world conditions.

What Are Attention-Based Contracts?

Attention-based contracts are agreements where payment, obligations, or future consideration depend on specific actions, performance outcomes, or conditions being met after the deal closes. As opposed to traditional fixed-price contracts, where value exchanges hands upfront, and risk is largely settled at signing, attention-based agreements tie part of the transaction to what happens later, often months or years into the future.

In business sales, these structures frequently appear as earnouts, milestone payments, deferred consideration, or performance-based pricing adjustments. They are made to bridge valuation gaps, protect buyers from overpaying, and encourage seller participation in post-sale success. But they introduce complexity because the seller’s final payout becomes contingent on results that may be influenced by market shifts or operational choices made by the buyer.

How Do These Contracts Shift Risk Between Buyers and Sellers?

Attention-based contracts redefine how risk is shared because they tie value to events or performance metrics that unfold after the deal closes.

Performance Risk Moves Toward the Seller

Earnouts and milestone-based payments tie compensation to future results. When revenue targets or operational benchmarks are not met, the seller receives reduced or no additional payment. Even strong performance can be affected by decisions the buyer makes after closing, such as changes in budget, staffing, pricing, or strategy.

Valuation Risk Moves Toward the Buyer

Buyers use attention-based contracts to avoid overpaying upfront. If the business underperforms or fails to integrate well, contingent payments naturally adjust downward. This protects the buyer from paying full value before the company proves its performance under new ownership.

Solvency and Timing Risk Moves Toward the Seller

Deferred payments or installment structures rely on the buyer’s long-term financial health. The seller may wait months or years for full compensation, extending exposure and reducing certainty compared to an upfront closing payment.

Operational and Control Risk Becomes Shared

Although both parties are involved in post-sale operations, the buyer ultimately controls decisions that influence earnout performance. This uneven control creates tension when outcomes affect the seller’s payout.

Advisors who understand these risk shifts help ensure sellers don’t unknowingly accept terms that limit control, reduce payout certainty, or create disputes after closing.

Implications for Sellers

Attention-based contracts often look appealing at first because they promise a higher total purchase price, but the details can significantly impact what a seller ultimately receives. When compensation depends on future milestones, the seller carries a meaningful share of performance and operational risk long after the deal closes. If targets are missed due to market conditions, integration issues, or decisions the buyer makes, the seller’s payout can shrink quickly.

Sellers also face reduced control once they hand over the business. Even if they stay involved temporarily, they no longer direct strategy, budgets, or staffing. Yet these very factors influence whether earnout or milestone goals are achieved. That imbalance can lead to disputes or unmet expectations if the terms were not clearly defined up front.

Another implication is extended financial exposure. Deferred payments and performance-based structures lengthen the seller’s dependence on the buyer’s solvency and commitment. A strong headline valuation can be misleading if a large portion is tied to uncertain future conditions.

Implications for Buyers

Attention-based contracts offer buyers meaningful protection, but they also introduce responsibilities that must be managed carefully. The primary benefit is reduced valuation risk. Instead of paying the full purchase price upfront, buyers can link part of the compensation to future performance. If the company underperforms, the buyer avoids overpaying, and the contract automatically adjusts the payout to reflect real results.

These structures also allow buyers to align incentives during the transition period. When sellers remain involved, performance-based payouts encourage them to support integration, maintain primary relationships, and help the business meet early milestones. This can stabilize operations and reduce the strain of change.

However, buyers must also recognize the operational and administrative burden that comes with contingent agreements. Earnouts require accurate tracking, clear reporting, and consistent communication to avoid misunderstandings. Ambiguous terms can lead to conflict, especially if the seller believes decisions made by the buyer hinder performance outcomes.

Buyers also assume integration risk. Even with strong targets, the business may face cultural, structural, or strategic challenges after acquisition. If the integration falters, it may delay progress and strain the relationship with the seller.

Information Asymmetry and Incentives

Information gaps sit at the center of attention-based contracts. Sellers typically know far more about the company’s day-to-day operations, customer behaviors, and hidden vulnerabilities than the buyer does. That imbalance creates risk on both sides. Buyers fear overpaying for performance that may not continue, while sellers worry that buyers might make post-acquisition decisions that reduce results and jeopardize their contingent payout.

Clear, objective performance metrics help narrow that gap. When both parties agree on how performance will be measured, reported, and validated, the contract becomes easier to manage and far less open to interpretation. Transparency around revenue sources, customer concentration, operational constraints, and historical performance patterns allows buyers to set fair expectations and gives sellers confidence that targets are achievable.

Data transparency also strengthens alignment. Well-defined reporting schedules, accessible dashboards, and shared documentation reduce suspicion and reinforce trust. With the right structure, incentives work with the transition rather than against it, ensuring both sides stay motivated and informed as the business moves through its early post-acquisition phase.

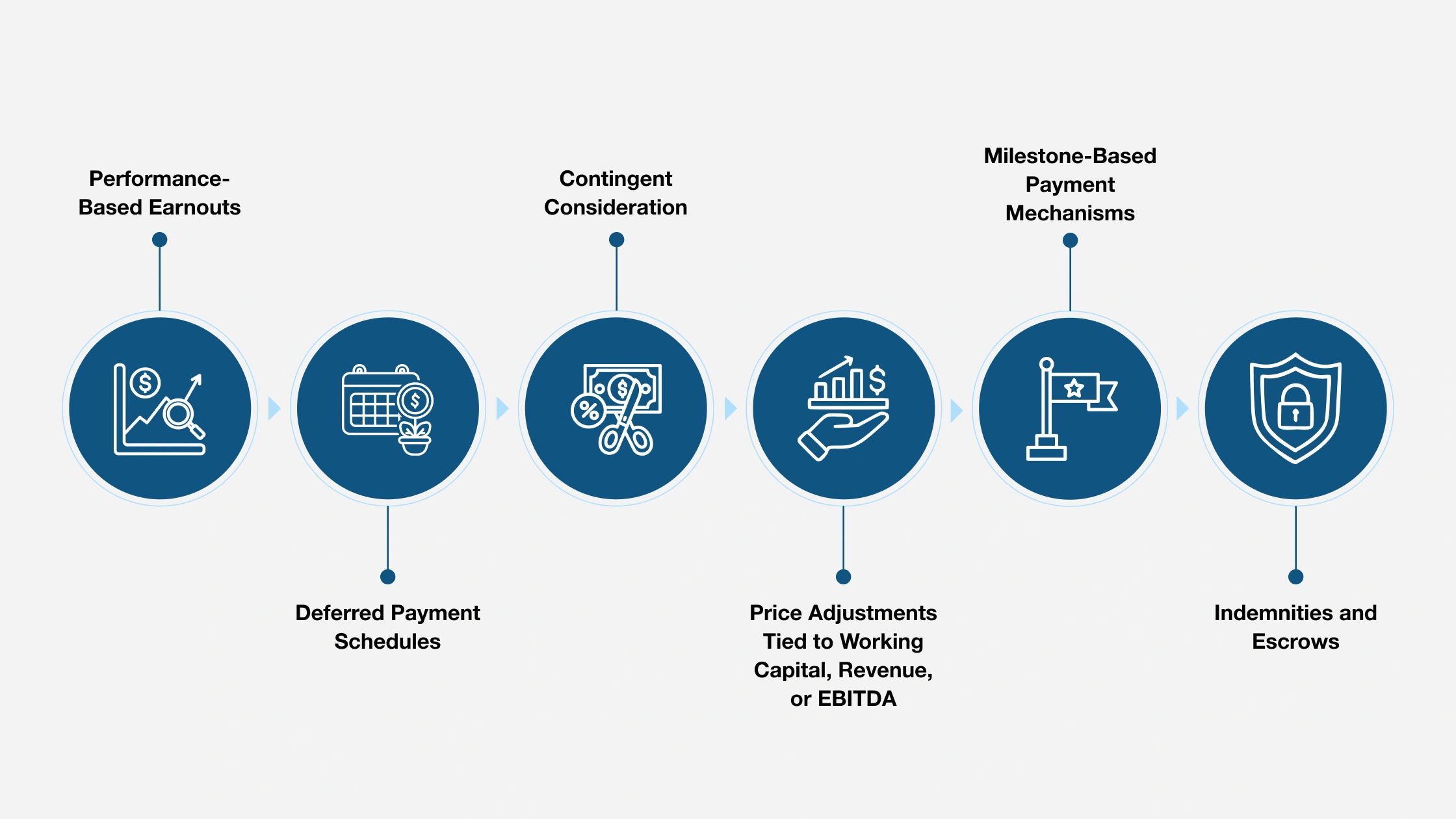

Contract Structures That Most Commonly Shift Risk

Attention-based contracts can take many forms, but several recurring structures tend to shape how risk moves between buyers and sellers. Each mechanism controls timing, payment certainty, and expectations in a different way. Understanding these structures helps both sides anticipate how value will ultimately be measured and delivered.

Performance-Based Earnouts

Performance-based earnouts tie part of the purchase price to post-acquisition results such as revenue, gross margin, or EBITDA. Buyers reduce upfront risk, and sellers stay motivated to support performance during the transition. The risk appears when metrics are unclear or post-sale changes make targets harder to reach.

Deferred Payment Schedules

Deferred payments spread out the purchase price over an agreed timeline. Buyers benefit from improved cash flow, while sellers gain predictable future payouts. The tradeoff for sellers is increased exposure if the business underperforms after closing.

Contingent Consideration

Contingent consideration structures adjust the final price based on agreed-upon future outcomes. These adjustments may relate to customer retention, key employee performance, or other measurable variables. Such structures balance risk, yet they demand precise definitions and consistent reporting.

Price Adjustments Tied to Working Capital, Revenue, or EBITDA

Working capital adjustments ensure the business maintains expected liquidity at closing. Revenue or EBITDA adjustments extend the concept by linking valuation to actual performance. These protections create fairness but require both sides to maintain clear documentation and transparent financial processes.

Milestone-Based Payment Mechanisms

Milestones tie payments to specific achievements such as product launches, approvals, or major client wins. This approach works well in industries where success depends on non-financial progress. It rewards sellers for hitting strategic goals and protects buyers from overpaying before those goals materialize.

Indemnities and Escrows

Indemnities and escrows safeguard buyers against unknown liabilities, including tax issues, contract disputes, or undisclosed obligations. Funds held in escrow cover potential claims. While this reduces risk for buyers, sellers accept delayed access to funds and must ensure complete disclosure to prevent disputes.

What Advisors Must Understand to Protect Owners

Advisors guiding business owners through attention-based contract structures must do more than explain terminology. They need a clear grasp of how these agreements redistribute risk, influence valuation, and impact the seller’s ability to realize the deal economics they expect. Owners often focus on headline purchase prices, yet the fine print determines how much of that value they actually receive.

Advisors who understand the mechanics behind these contracts can prevent misunderstandings, anticipate points of friction, and negotiate protections that keep owners aligned with their goals.

Advisors should evaluate how performance metrics are defined, measured, and monitored. They must understand operational changes a buyer might make post-closing that affect earnout targets or milestone achievements. Advisors also need to anticipate information asymmetry, ensuring owners are not placed at a disadvantage once control shifts.

Reviewing reporting obligations, dispute resolution pathways, and mechanisms for transparency helps protect sellers from unexpected outcomes. The strongest advisors ground owners in a realistic view of potential outcomes so expectations remain clear and achievable throughout the transition.

How IEPA Prepares Advisors to Manage Risk-Shifting Contracts

Attention-based contracts demand a level of analysis and negotiation skill that many advisors never formally develop. Structures like earnouts, contingent payments, milestone triggers, and price adjustments require advisors to interpret financial, operational, and behavioral factors simultaneously.

IEPA’s Certified Business Exit Consultant® (CBEC®) program equips advisors with the practical resources and transaction experience needed to guide owners through these complex agreements with clarity and confidence.

CBEC® candidates learn how risk shifts between buyers and sellers, how to recognize hidden vulnerabilities within contract structures, and how to negotiate terms that safeguard the owner’s financial outcome. Training emphasizes real-world case studies, scenario modeling, and deal mechanics so advisors understand how post-close decisions, reporting changes, or operational shifts can impact contingent payouts.

The program also reinforces the importance of aligning incentives, clarifying performance metrics, and designing contracts that remain fair and workable long after control transfers.

Advisors who complete the CBEC® program bring owners a higher level of preparedness, one rooted in practical insight, and that expertise can be the difference between a transition that goes smoothly and one that unravels under pressure.

Advance Your Skillset With the CBEC® Certification from IEPA

Advisors who guide owners through attention-based contracts must be prepared to interpret complex deal structures, anticipate risk shifts, and negotiate terms that protect long-term value. The CBEC® certification gives you that edge. IEPA’s practitioner-led program delivers practical training built around real transaction scenarios, so you can confidently support owners through deals where earnouts, contingent payments, and incentive-linked structures shape the final outcome.

CBEC® certification helps advisors stand out in a growing market:

- More than two-thirds of CBEC® advisors serve Main Street and Middle-Market owners, reinforcing the depth of practical, transaction-focused experience cultivated in the program.

- 66 percent of CBEC® advisors structure engagements across multiple phases, strengthening long-term client relationships and increasing advisory impact.

- 22 percent of CBEC® professionals earned over $250,000 from exit planning services in 2024, demonstrating the financial strength of building a practice around real exit planning expertise.

Advisors who master attention-based contracts help owners protect the outcomes they’ve spent a lifetime building. Elevate your capabilities and join a community committed to Exit Planning excellence.